By Olukemi Odoh

- Abducted Oyo Pupils, Teachers Rescued After 56 Days in Captivity

- First Batch of Evacuated Nigerians Arrive Home from South Africa Amid Xenophobic Tensions

- Food and Beverages West Africa Exhibition Set for Landmark Event Centre This June

- Interview: Naira Stability May be Tested By Global Oil Crisis.

- Customs to End Routine Physical Cargo Inspection By December.

In a bid to fortify Nigeria’s banking sector and position it for deeper financial intermediation, greater resilience, and broader economic support, the Central Bank of Nigeria (CBN) initiated a sweeping bank recapitalisation exercise that has been unfolding since 2024. This regulatory reform represents one of the most consequential overhauls of the financial system in more than a decade, affecting virtually every deposit-taking bank operating in the country. The directive sets new minimum capital requirements that banks must meet based on their licence categories, with a compliance deadline of March 31, 2026.

Why Recapitalise? The Rationale Behind the Reform

Recapitalisation is the process by which banks increase their core capital base — primarily through raising fresh equity, private investment, rights issues, bond issuances, mergers or other strategic transactions — to meet regulatory minimums. In March 2024, the CBN revised the minimum capital thresholds to reflect the evolving size and complexity of the Nigerian financial system and the need for stronger buffers against economic shocks.

Under the new framework:

- Banks with international commercial licences must hold a minimum capital of ₦500 billion (up from much lower pre-existing thresholds).

- National commercial banks are required to have at least ₦200 billion.

- Regional commercial banks must reach ₦50 billion.

- Non-interest banks and merchant banks have proportionate, tiered requirements.

These higher benchmarks aim to achieve several key objectives:

- Enhance resilience of banks to absorb economic shocks and manage risks better.

- Expand capacity to finance large-scale projects, particularly in critical sectors like infrastructure, energy, and industrial production.

- Boost investor confidence and attract foreign capital into Nigeria’s financial markets.

- Support Nigeria’s broader economic goals, including efforts to grow GDP, deepen capital markets, and achieve a more diversified economy.

The policy also aligns with Nigeria’s transition toward Basel III standards — global regulatory norms that emphasise stronger capital and liquidity frameworks — though local requirements and timelines remain subject to CBN discretion.

The March 2026 Deadline

The CBN announced the recapitalisation policy in March 2024 and gave banks about two years to complete the process — setting March 31, 2026 as the final deadline for compliance.

As the deadline approaches, there has been increasing regulatory urgency and market attention on how individual banks are progressing. The CBN has emphasised an orderly and transparent process while reinforcing that non-compliance could result in sanctions, licence downgrades, forced mergers, or other regulatory interventions.

Who Has Met the Recapitalisation Requirements So Far?

Reporting on compliance has evolved over time, reflecting real-time progress across the banking industry:

- Mid-2025, only a handful of banks had met the requirements, with eight banks fully compliant by July 2025.

- By September 2025, that figure had grown to around 14 banks having met the new capital benchmarks.

- By November/December 2025, the CBN confirmed that 16 banks had fully met the recapitalisation threshold.

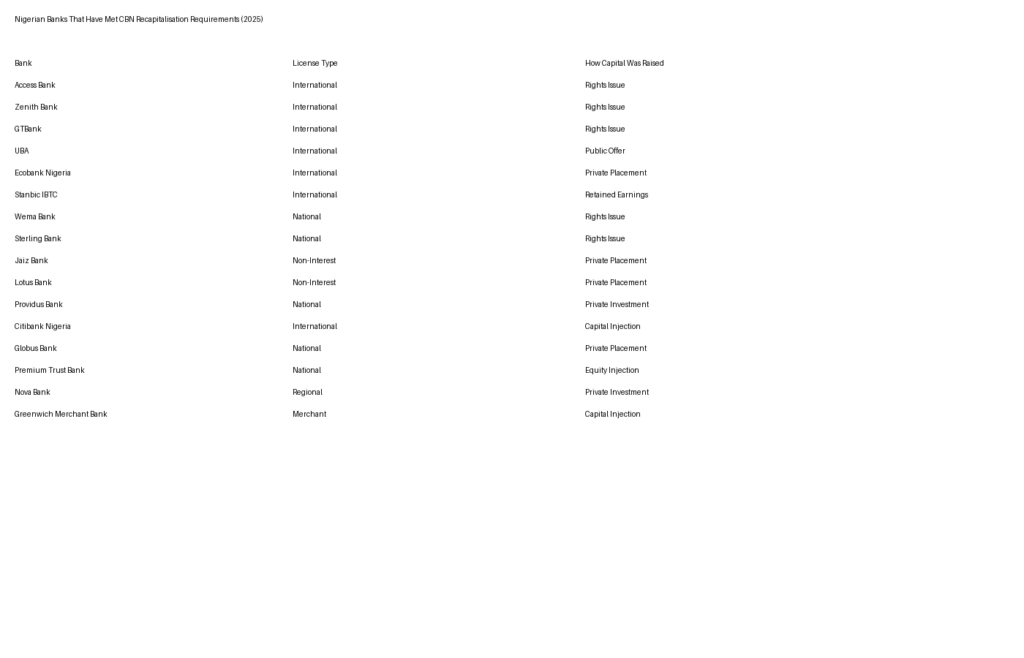

These compliant banks span various licence categories and represent both domestic and international players. According to industry sources, the list of banks that have met or exceeded the new capital requirements includes:

- Access Holdings / Access Bank

- Zenith Bank

- Guaranty Trust Holding Company (GTBank/GTCO)

- United Bank for Africa (UBA)

- Ecobank Nigeria

- Stanbic IBTC Bank

- Wema Bank

- Jaiz Bank

- Lotus Bank

- Providus Bank

- Greenwich Merchant Bank

- Premium Trust Bank

- Globus Bank

- Citibank Nigeria

- Sterling Bank

- Nova Bank

These institutions have leveraged various strategies to bridge the capital gap, including:

- Rights issues and public share offers, allowing existing shareholders and the public to invest more capital.

- Private placements and bond issuances targeted at institutional investors.

- Strategic mergers and acquisitions, notably the merger of Union Bank with Titan Trust Bank, which created a combined entity that satisfied capital requirements.

For several major banks, particularly those with international licences, rights issues have been a dominant tool. For example, Access Bank raised hundreds of billions of naira through a rights issue, helping it cross the ₦500 billion threshold early in the exercise.

Banks Still Working to Comply

Despite the notable progress, not all institutions have fully met the recapitalisation targets. As of late 2025, many banks have raised capital — with 27 additional banks actively engaged in capital-raising efforts — but are still in the process of meeting regulatory standards ahead of the March 2026 deadline.

Among these are several banks that had not yet filed final compliance reports or whose capital increases were still undergoing regulatory review. These banks are utilising a mix of rights issues, private placements, potential mergers, and strategic partnerships to shore up their balance sheets.

For some mid-tier and regional banks with smaller investor bases, attracting fresh capital at scale poses a challenge, and market analysts have noted that this could catalyse further consolidation in the sector as weaker institutions seek mergers or acquisitions to survive the reform.

- Abducted Oyo Pupils, Teachers Rescued After 56 Days in Captivity

- First Batch of Evacuated Nigerians Arrive Home from South Africa Amid Xenophobic Tensions

- Food and Beverages West Africa Exhibition Set for Landmark Event Centre This June

- Interview: Naira Stability May be Tested By Global Oil Crisis.

- Customs to End Routine Physical Cargo Inspection By December.

How Banks Are Meeting the Requirements

Bank recapitalisation is not merely a regulatory hurdle; it is also a strategic exercise that impacts corporate ownership, investor relations, and future business models. The main channels through which banks are meeting the CBN’s capital targets include:

- Rights Issues: A large number of compliant banks ran successful rights issues, offering shares to existing shareholders to raise equity. Access Bank’s ₦351 billion rights issue is a prominent example.

- Public Offers: Some banks tapped the public capital markets by offering new shares to outside investors.

- Private Placements: Private sales of equity to institutional investors or strategic partners helped several banks quickly boost their capital base.

- Mergers and Strategic Combinations: As seen with Union Bank and Titan Trust Bank, combining balance sheets can expedite compliance and create more competitive institutions.

The recapitalisation exercise has broader implications beyond bank balance sheets. By strengthening the capital base of the banking sector, the CBN hopes to:

- Increase lending capacity to businesses, particularly in sectors that require sizeable financing.

- Enhance risk-absorbing capacity amid volatile macroeconomic conditions.

- Encourage foreign and domestic investment into the financial sector and wider economy.

- Support stability in the face of inflationary pressures, currency volatility, and global financial shocks.

The reform also coincides with other CBN initiatives aimed at promoting monetary stability and transitioning Nigeria’s financial sector toward international regulatory best practices.

Nigeria’s bank recapitalisation exercise stands as a landmark regulatory initiative designed to ensure that its financial system remains robust, competitive, and capable of supporting national development goals. With the March 31, 2026 deadline fast approaching, 16 banks have already met the new capital requirements through strategic capital raising and structural transactions, while several others are actively working toward compliance.

As banks close the final stretch of this compliance race, the exercise is expected to leave Nigeria’s banking industry with stronger balance sheets, improved resilience, and an enhanced ability to finance the country’s ambitious economic agenda in the years ahead.

- Abducted Oyo Pupils, Teachers Rescued After 56 Days in Captivity

- First Batch of Evacuated Nigerians Arrive Home from South Africa Amid Xenophobic Tensions

- Food and Beverages West Africa Exhibition Set for Landmark Event Centre This June

- Interview: Naira Stability May be Tested By Global Oil Crisis.

- Customs to End Routine Physical Cargo Inspection By December.